Accurate Cost Calculation: Tracking Actuals vs. Standard Costs

For many CFOs and financial controllers in manufacturing, the end-of-month close is a moment of reckoning. It is the moment when the “Standard Cost”, the estimated cost used for pricing and budgeting, meets the “Actual Cost”, the reality of what happened on the shop floor.

When these two numbers drift too far apart, margins erode silently. In a volatile market, relying on annual standard cost estimates is a financial risk; you need the agility of real-time actuals.

To protect your bottom line, you must move beyond spreadsheets and adopt dynamic manufacturing cost calculation.

Table of Contents:

- The Trap of Standard Costs

- The Manufacturing Cost Calculation Formula: Theory vs. Reality

- Beyond Direct Costs: Handling Overhead and Allocation

- A Manufacturing Cost Calculation Example

- How Nexelem Bridges the Gap

The Trap of Standard Costs

Standard costing is a proper accounting convention. It assumes a stable environment: material prices are fixed, machine cycle times are constant, and energy costs are predictable.

However, the factory floor is rarely stable. A machine breakdown might force you to switch to a less efficient legacy machine. A rush order might trigger overtime pay. A supplier issue might force you to buy premium raw materials.

If your manufacturing cost calculation software only tracks the standard, you are blind to these variances until the P&L statement arrives. You might be selling a product at a loss, believing it is profitable, simply because the actual labor and overhead consumed were higher than the standard model predicted.

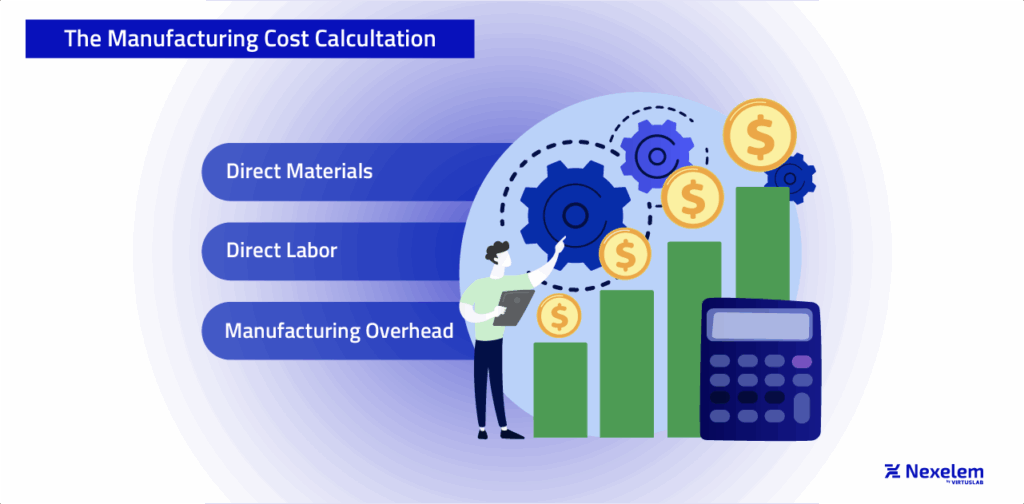

The Manufacturing Cost Calculation Formula: Theory vs. Reality

At its simplest, the manufacturing cost calculation formula is:

Total Cost = Direct Materials + Direct Labor + Manufacturing Overhead

While the formula is simple, capturing the data to feed it is complex.

- Materials: Did you account for the 5% scrap rate on Tuesday?

- Labor: Did the operator spend 3 hours or 4 hours on the batch?

- Overhead: How do you allocate energy costs when machine utilization fluctuates?

Without real-time data, this formula is populated by guesses. To get accurate actuals, you need to integrate your financial view with your operational data.

Beyond Direct Costs: Handling Overhead and Allocation

One of the most significant “blind spots” in traditional costing is the allocation of overhead. Many companies apply a “peanut butter spread” approach, assigning a flat overhead rate across all products. This approach distorts profitability.

For instance, Product A might require a high-energy furnace and constant supervision, while Product B requires simple manual assembly. If you apply the same overhead rate to both, Product B effectively subsidizes Product A. Accurate manufacturing cost calculation software prevents this cross-subsidization.

By tracking specific machine run-times and energy consumption per work order, you can allocate indirect costs with surgical precision. This allows you to identify which products are truly driving your utility bills and maintenance costs, giving you the data needed to adjust pricing or re-engineer the process.

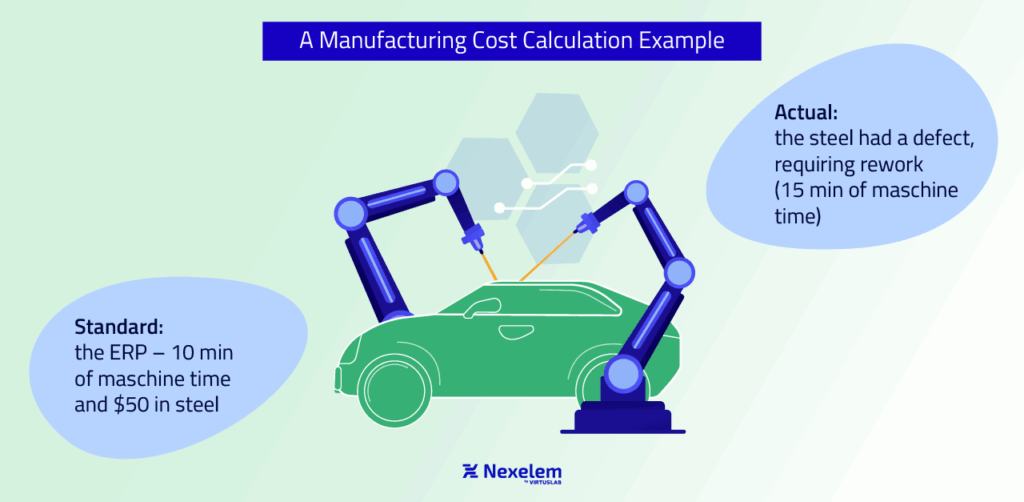

A Manufacturing Cost Calculation Example

Consider a manufacturer producing an automotive component.

- Standard: The ERP says it takes 10 minutes of machine time and $50 in steel.

- Actual: The steel had a defect, requiring rework. The machine ran more slowly due to a worn tool, taking 15 minutes.

In a standard model, the cost remains $X. In a dynamic model, the cost spikes to $Y. If you have visibility into this variance immediately, you can investigate the root cause, the worn tool, rather than just absorbing the loss at the end of the quarter.

This is where precise tracking of OEE (Overall Equipment Effectiveness) becomes a financial tool, not just an operational one. It explains why the costs were higher.

How Nexelem Bridges the Gap

Nexelem moves cost calculation from “post-mortem analysis” to “live monitoring.” By tracking production in real time, Nexelem captures the exact labor hours, machine time, and material usage for each work order.

This creates a feedback loop. You can compare the theoretical cost against the actual cost instantly. This granular visibility empowers CFOs to make data-driven decisions on pricing, sourcing, and capital investment. It transforms cost accounting from a compliance task into a strategic advantage for reducing production costs.

Stop guessing your margins. Gain complete control over your financials with Nexelem’s comprehensive manufacturing platform.